First Time Buyers Are Back

Could the first time buyers property market finally be starting to shake the stagnancy it’s been suffering for the past decade or so and finally start moving again?

From figures revealed by the trade body UK Finance, it looks like it. And the reason? First-time buyers are back! The market has always needed the ‘bottom rung of the ladder’ to move in order to keep the rest of it flowing. But until last year that wasn’t happening.

Number of first-time buyers reach pre-recession rates

Now the statistics show things are really starting to look up. That’s because in 2018 there were 370,000 new first-time buyers in the UK. If that sounds familiar to those who’ve been around in the property market for a few decades then it’s not surprising – because 370,000 new first-time buyers were typically the number we were looking at prior to the recession in 2006. The figure then was, in fact, 402,800 first-time mortgages, showing the 2018 number wasn’t too far behind.

Last year’s first-time buyer mortgage figure was also 1.9 per cent up on the previous year – showing that government initiatives to jolt the market may indeed finally be trickling through and having their desired effect. These include Help to Buy, Shared Ownership schemes, stamp duty exemption, family-link mortgages and fewer landlords so more available properties.

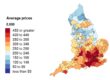

First-time buyers in the West Midlands are taking out mortgages for around £168,000. In the East Midlands, it’s an average £163,005. For first-time buyers in Greater London, it’s a completely different story; they’re looking at an average mortgage of £422,000. Meanwhile, the figure for the typical first-time buyer mortgage in the UK as a whole is more than £212,000.

And, as for the age of those first-time buyers? It’s risen over the past four decades – but not by much. In 1977 it was 27, in 2017 it has risen to 30, according to the UK cities house price index Hometrack. In London, the typical first-time buyer age is 31.

Low – or ‘No – deposit first-time buyer deals becoming commonplace

High Street lenders have also been keeping mortgage rates low for high loan-to-value deals – to the extent, there is now 46 per cent more 95 per cent mortgages than there was just one year ago. That’s according to recent research by consumer rating company Defaqto. ‘No deposit’ mortgages have also become a thing – where a family member ends up as a guarantor of sorts by contributing a percentage of the loan. Lloyds, Barclays and Nationwide all offer variations on this. Others, such as Aldermore Bank and Family Building Society, ask for parents or other close family members to use their own homes as security rather than a deposit. But deals like this really aren’t surprising when you consider that the average first-time buyer deposit has jumped from £1,094 in 1977 to £25,867 in 2018!

Meanwhile, actual lending by banks for first-time mortgages in 2018 amounted to £62 billion in 2018 – a 4.9 per cent increase on the previous year. The market is currently showing more than 17,000 first-time buyer mortgage products.

First-time buyers should carefully consider locations

Meanwhile, sticking with the West Midlands, if a report issued by Hometrack earlier this month is anything to go by then first-time buyers should be heading for Birmingham where, the site forecasts, property prices are expected to increase by up to 30 per cent over the next four years. Other cities set to benefit, says the company, are Edinburgh and Manchester. All three cities are enjoying high house inflation; Birmingham has 7.3 per cent with Manchester 6.7 per cent and Edinburgh highest at 7.7 per cent.

Interested in investing in property in Birmingham or Manchester? Then do get in touch, call 0121 573 0133 or fill out the contact card below